China's Healthcare and Biotech

- Angela Yu

- Aug 31, 2019

- 11 min read

With China’s health care industry projected to be worth $2.4 trillion by 2030, there has been growing interest from domestic and foreign investors in the field. In this report, we investigate the the industry's upward trajectory by providing a comprehensive market overview and case studies.

TABLE OF CONTENT:

China’s Healthcare System

- Demographics

- Fertility

- Nursing homes

- Chronic diseases

- Healthcare Insurance

- Disease screening

China Health Care Market Overview

- Growing Healthcare Expenditure

- Increased Market Access

- New China Rare Disease List

- Accelerated Drug Approval Process of CFDA

Channels for US Company to Enter

- Licensing Agreement

- Collaboration with Chinese Companies/Launch Sister Companies Focusing on Chinse-specific Diseases

- Participating in a Broader Healthcare Ecosystem

- Potential to Tap Into the Digitization of the Healthcare Industry

Established US Biotech Company in China

- Eli Lily

- Illumina

PART ONE: China’s Healthcare System

Demographics:

Key statistics:

1. Total Population: 14.3 Billion as in 2019 (source: United Nations projections)

2. Projected population growth: 0.6%

3. 60.4 % of the population is urban in 2019

Urban population growth (unit: 10k)

4. China’s aging population is expected to increase the burden of chronic disease by 40% by the year 2030

5. By 2053, China will have 487 million senior citizens, making up 35% of the total population

Senior population(>65) (unit: 10k)

Infertility:

Currently there are more than 40 million infertile people in China, infertility rate has risen from 3% 20 years ago to about 15% in recent years

In 2017, there are 2705 infertile women per 10 thousand women and 878 infertile men per 10 thousand men

Increasing pregnancy rate of older women 0.86% in 2003 to 1.86 % in 2015

Assisted reproductive technology:

Artificial insemination and IVF are two major types of assisted reproductive technology, with an estimated annual case 5 million

Market size: 118 billion RMB

The clinical pregnancy rate is about 40%, and the delivery rate of live infants is 30%-35%

451 reproductive centers in 2016; the total number of reproductive centers in China caps at 550 (Ministry of Health); the average growth rate is 20 per year

IVF licensing hard to obtain (price of license approximately 0.5-1 billion in tier one cities); 91% of licenses held by public reproductive centers

Industry in serious shortage of supply; gross profit margin is close to 70% and net profit margin is 30%

Public-traded companies entering industry: 通策医疗 (the only IPO company with reproductive center licence; financial deficit from 2015 to 2018) 锦欣生殖 (HKG)

Nursing home:

Number of nursing homes in China has more than tripled in the past five years, according to the Ministry of Civil Affairs; currently, nursing homes are sponsored by the government of China with contributions from some nongovernment organizations and private investors

More than 28000 nursing institutions as of 2018,

There currently is a shortage: for every 1000 senior citizens, there are only 31.6 nursing home beds

Problem:

“surging demand and limited affordability” -- hard for foreign nursing home operators to make a profit

1. In 2012 the average annual disposable income for an urban Chinese was 24,600 yuan, while the average price for a bed in a nursing home was 42,400 yuan

2. Aging mainland Chinese mostly rely on the sparse government pension and their children’s care for their retired life

3. absence of tailored insurance schemes prevent elders from spending money on health care

Suboptimal care and lack of carer training

Chronic Disease:

1. Leading Cause of Death by Gender

2. Leading Cause of Death by Age group:

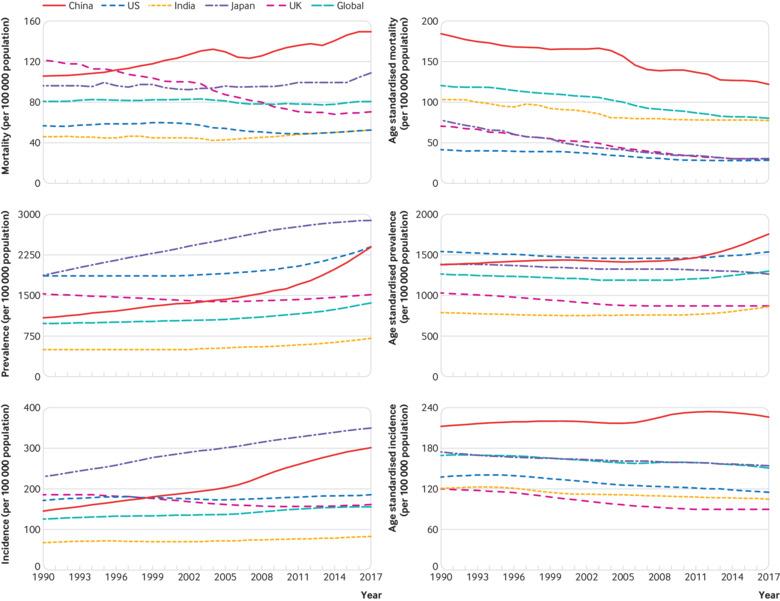

3. Cancer:

China has a cancer survival rate less than half that of the United States (five year survival rate of all cancers in China is 30.9 percent; US: 66 percent)

3.12 million people are diagnosed with cancer per year (rate which has doubled over the past two decades)

Favorable Policies:

A zero tariff policy on a range of anticancer drugs and other pharmaceuticals made overseas

Government procurement of seventeen anticancer drugs had amounted to 562 million yuan (62 percent overall drop in price).

Including the drugs in the national reimbursement list under the basic medical insurance scheme reduce patients’ out-of-pocket payment by more than 75%

4. Vascular Disease:

Stroke is the leading cause of death in China, with the country accounting for roughly one third of worldwide stroke mortality

Aging is the most significant contributing factor

China Cardiovascular Association developed program to promote healthy lifestyles through educational activities focusing on modifiable risk factors such as smoking and lack of exercise

Problems:

Suboptimal rehabilitation: data from 2012-13 showed that only 59.4% of patients with stroke received rehabilitation assessment during hospital admission, and only half of these were assessed by a rehabilitation therapist (reason: lack of insurance coverage, lack of rehabilitation system, less developed technology)

Unintegrated care and healthcare information systems: chain from emergency service system to designated stroke centres, multidisciplinary organisation, and discharge to community hospital or rehabilitation centre is weak

From the plot: age-standard mortality/incidence is well above global average;

age standard prevalence is on the rise

HealthCare Insurance

Composition

Basic Medical Insurance (covers 95% of the population):

Urban employment-based basic medical insurance

mandatory for employees in urban areas

Insured 283.3 million in 2014 (20% of the population)

Financed mainly from employee and employer payroll taxes, with minimal government funding

Employers contribute 6%–12% of the employee’s salary to the fund depending on the province, while the employee contributes 2%

Administered by the Ministry of Human Resources and Social Security and run by local authorities

Urban resident basic insurance

Voluntary at the household level, covered self-employed individuals, children, students, and elderly

Insured 314.5 million in 2014 (23%)

Financed by local and provincial government

Administered by the Ministry of Human Resources and Social Security and run by local authorities

The new rural cooperative medical insurance

Voluntary at the household level in rural areas

Insured 736 million in 2014 (54%)

As of 2011, the enrollment rate was 97.5%

Financed mainly by government

Administered by the National Health and Family Planning Commission and run by local authorities

Private/commercial health insurance:

Primarily purchase by higher-income individuals and by employers

Provides a better quality of care, higher reimbursement, and services and medicine that are not covered by public insurance

Landscape of private health insurance in China

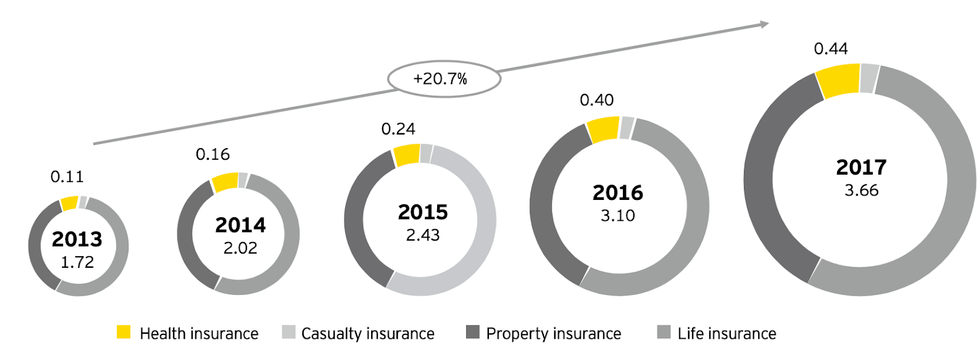

Chinese current commercial insurance market is dominated by life insurance and property insurance. Although health insurance has a small market share, it has the highest growth rate with high potential in the future.

In 2017, China’s gross original premium income of the whole private insurance market was RMB 3.66 trillion. It has been growing steadily with a 4-year CAGR of 20.7%. The original premium income of health insurance was RMB 0.44 trillion, with a 4-year CAGR of 41.4%.

China’s private insurance industry is dominated by life insurance, accounting for 58.7% of the original premium income, and property insurance, 26.9%. Health insurance accounts for only 12%.

In 2018, health insurance has the highest yoy compared with other insurances.

In 2018, gross original premium income of life insurance was RMB 2.073 trillion, yoy -3.41%; premium income of property insurance was RMB 1.077 trillion, yoy +9.51%; premium income of health insurance was RMB 0.545 trillion, yoy +24.12%; premium income of casualty insurance was RMB 0.108 trillion, yoy +19.33%

The health insurance market is highly concentrated and dominated by Chinese-funded life insurance companies

Health insurance is currently sold through life or property insurance companies, with life insurers taking the major share of the market

(Life insurance share of the total health insurance premium income in 2017)

China’s Private Health Insurance Provider

Domestic Provider

International healthcare providers usually cater to the needs of expats.

Disease Screening

AI and Disease screening: China’s DNA sequencing market, worth about $1.05 billion USD in 2018, is forecast to grow to 2.6 billion USD in 2022, (estimates by Beijing-based CCID Consulting).

DNA Sequencing Kit:

23Mofang is the largest of more than a hundred companies in China currently offering genetic testing services to consumers (Other big players: WeGene, Novogene and 360°Gene); Shipments of DNA sequencing machines to China from American company Illumina rose by 42 percent last year.

Tests include genes linked to one’s tendency to sweat, hypertension risk, pain tolerance, and long-term memory capacity

HK Genome Project:

Entire genetic code decrypted of tens of thousands HKers for building database to boost diagnoses of rare illnesses and aid cancer treatment

Researchers can access the anonymised data for cancer studies and how genes affect person’s response to drugs

Aim to diagnosing uncommon disorders and developing more personalised treatment for cancer patients.

2. DNA Sequencing

Automatic data mining from electronic medical records, laboratory testing reports, imaging materials, life-style data, and social media data, etc.

Building forecasting models to automatically predicting disease possibility (removes human error)

Mature Technology: Qure.ai for identify and localize abnormalities on X-rays, MRI and CT scans

Ruining Zhitang working with Shanghai hospital achieves 88pc accuracy rate in tests predicting diabetes 15yr in advance (using information from 170,000 people)

YituTech launched “AI Anti-Cancer Map” (AI 防癌地图)in conjunction with several top medical institutions in China aiming to expand the service supply capacity of cancer screening using AI (project fund: 100 million RMB)

Guangxi gov supported project “Early Cancer Screening in Digestive Tract” targeting low income group with high risk (using Tencent Miying AI)

PART TWO: China Health Care Market Overview

Growing Healthcare Expenditure

According to All China Health Care Index in 2018, China is one of the fastest growing major healthcare markets in the world with a 5 year compound growth of 11%, compared to 4% in the U.S. and -4% in Japan. It currently is the second largest healthcare market globally.

Increased Market Access

Market access improved significantly in the past few years: 181 drugs were added to the national reimbursement drug list (NRDL) in two rounds of updates since 2017; in addition, 187 were added to the essential drug list (EDL) in 2018, six years after the previous update. Experts are optimistic about the possibility of more frequent NRDL updates every year or two, and even more frequently at the level of patient groups or therapeutic areas, such as pediatrics or rare diseases.

New China Rare Disease List

In 2018, the list includes 121 diseases covering various genetic disorders; some diseases on the CNDA list are not in the FDA database. The list shows that China is not only interested in bringing in existing treatments, but is also preparing to lead orphan drug development in certain areas in the future.

* An orphan disease is defined as a condition that affects fewer than 200,000 people nationwide.

Development of Acceptance for Oversea data for Orphan Drug:

On June 20, 2018, the State Council issued that orphan drugs can be approved with overseas clinical data only if certain conditions are met, and that the CNDA shall review the application within 3 months. This not only adds a clear review timeline to the regulatory pathway, but it also promises to accelerate approvals significantly. Moreover, rare disease drug can gain approval with overseas clinical data regardless of whether the drug has been approved in other countries or not. This means it is potentially possible to file applications for new orphan products simultaneously in China and other regions.

Accelerated Drug Approval Process of CFDA

In 2016, CFDA created priority review status for certain innovative drugs, reducing review times to six months.

In 2017, China further loosened restrictions by allowing Chinese-produced generics as well as imported innovator drugs to apply for approval without the need for full clinical trials performed within China.

PART THREE: Channels for US Company to Enter

Licensing Agreement:

In 2018, Chinese biotechs made 164 cross-border licensing deals, more than double the number five years ago, according to consultancy China Bio. Such deals accounted for most of the $13.8bn that Chinese pharmaceutical groups spent on licensing agreements. Chinese Venture Capital firms are on the hunt to find drug candidates at a pre-clinical stage for them to develop and commercialise, which provides a vital route for European and US biotechs.

Case Study:

Shanghai-based Everest Medicines paid US peer Immunomedics $65m for the China rights to a cancer drug, followed by another $60m payment if the medication is approved in the US and up to $710m further depending on its sales. Agreement sets a new benchmark for a single-asset licensing deal for regional China.

Zai Lab, another Shanghai biotech company paid $20m for rights in greater China to a cancer drug candidate developed by US-based Deciphera, which will be eligible for further payment of up to $185m if the drug is successfully commercialised.

Britain’s ReNeuron, which develops stem-cell treatments for eye disease and strokes, is set to receive £80m plus royalty payments from China’s Fosun Pharma for the rights to two treatments.

Collaboration with Chinese Companies/Launch Sister Companies Focusing on Chinse-specific Diseases

Case Study:

China’s BeiGene teamed up with SpringWorks Therapeutics to develop therapeutics that will target advanced solid tumors that contain RAS mutations

WuXi formed a partnership with Seattle-based Juno Therapeutics to develop treatments for cancer using Juno’s chimeric antigen receptor (CAR) and T cell receptor (TCR) technologies in combination with WuXi AppTec's R&D and manufacturing platform.

Roivant Sciences launched Sinovant Sciences in China with an aim at developing innovative treatments for some of China’s most pressing medical concerns such as liver cancer and drug-resistant bacterial infections.

Participating in a Broader Healthcare Ecosystem

Opportunity for VC to connect startups with hospital/government to create integrated environment.

Case Study:

AstraZeneca has set up centers for chest pain, metabolic management, and pulmonary care, for example. By joining forces with government stakeholders, academic institutions, digital and tech companies, device manufacturers, hospitals, and key opinion leaders, AstraZeneca is able to provide better integrated solutions for patients and clearer value propositions for hospitals and clinicians. In 2018, AstraZeneca achieved 25 percent growth in China, reaching some $3.8 billion in total sales.

Potential to Tap Into the Digitization of the Healthcare Industry

China has the potential to lead the digitization of the industry because of its policy tailwinds, acute need for new solutions, and strong digital ecosystem. Many leading private digital companies (including JD, Tencent) are already putting healthcare on their strategic agendas such as online diagnosis and treatment, patient support and drug tracking.

Tencent:

network of participating hospitals – over 38,000 medical facilities as of 2017: users can book doctor’s appointments through their WeChat Intelligent Healthcare)

Following their health checkup, patients can access their medical reports through WeChat and pay for their medical bills.

Wechat step count function can be linked to WeSure. (Red packet as incentive)

Pingan Hao Yisheng

one-stop healthcare ecosystem platform, piloted unstaffed clinics that employ artificial intelligence called “One-minute Clinics” near Shanghai, (connect patients with a clinician on Ping An Good Doctor’s in-house medical team)

In January 2019, the company had placed its One-minute Clinics across 8 provinces and cities in China and signed service contracts for nearly 1,000 units, providing healthcare services to more than 3 million users.

SUNPA

Built four Telemedicine centers in China in cooperation with public institutes. (covers eight provinces and municipalities with a total population of over 200 million)

Ping An Insurance

Pushing for a national telemedicine network.

Offering a simple app to order non-prescription medicine and personal care products online. (complete a quick, AI-driven questionnaire for the app to determine their health needs, product delivered in an hour

PART FOUR: Established BioTech Firms

Eli Lily

China’s Pharma Market:

China was the world’s second-largest national pharmaceutical market in 2017 — worth $122.6 billion.

It is also the biggest emerging market for pharmaceuticals with growth tipped to reach $175 billion by 2022.

History and Development:

Since returning to China in 1993, Lily now has more than 3,000 employees, reaching nearly 400 cities in China.

Built strategic partnerships with more than 10 local companies and academic institutions since the late 1990s.

Developed products that take leading roles in many therapeutic areas include endocrine, central nervous system and oncology, etc.

fThe company’s innovative medicines like Prozac®, Zyprexa® are widely used in the medical practices in China.

Recent Partnership with Local Entities:

Partnered with China‘s National Center for Cardiovascular Diseases to develop cardiovascular disease risk calculator; Lilly will have access to data from more than one million people in China with type 2 diabetes and increased CVD risk.

Sold the rights of two legacy antibiotic medicines, Ceclor® and Vancocin®, as well as a manufacturing facility in Suzhou, China that produces Ceclor, to a China-based specialty pharmaceutical company Eddingpharm for $350 Million.

Partnered with Chi-Med to commercialize the first home-grown, China-discovered and developed drug Elunate.

Illumina

China’s DNA Sequencing Market:

China’s DNA sequencing market, worth about $1.05 billion USD in 2018, is forecast to grow to 2.6 billion USD in 2022, (estimates by Beijing-based CCID Consulting).

History and Development:

China has already become Illumina‘s largest market outside the United States, and genome sequencing data are widely used in key sectors such as agriculture, forensic science and clinical operation in China.

Illumina reported $185 million in revenue from China, Taiwan and Hong Kong—about 11% of the company’s total in the first half of 2018. Shipments also rose 42 % compared to the same period in 2017.

Recent Partnership with Local Entities:

In 2018, Illumina received the first official Chinese government clearance for one of its next-generation sequencing systems, allowing the company to market and sell its own benchtop MiSeqDx device to hospitals and other institutions.

Illumina launched its BaseSpace cloud-based sequencing hub in China in January, 2018, providing data storage, management and analysis services to local Chinese businesses.

Next step aims to team up with Chinese startup companies in China’s genome sequencing service sector, such as DNA tracking to increase global footprint

PART FIVE: Conclusion

Some of the driving forces behind China healthcare's unprecedented growth lie in the improvements in infrastructure, the broadening of insurance coverage and significant support for innovation. However, the recent political impact of CFIUS might pose substantial challenges to ride on the wave of China's development. How to leverage China's growth under precent turbulent state remains key to the decision making process of domestic and foreign investors alike.

Reference:

Comments